When it comes to financing real estate investment, conventional loans are not your only option. There is also a DSCR loan Colorado. Compared to their conventional counterparts, DSCR loans are more flexible, easier to qualify for, and excellent for investors in many diverse situations.

In this post, we explain everything you need to know about DSCR loans. We start with its definition, then we explain what and who these loans are for. Finally, we explain the documentation requirements you need to prepare to qualify for a DSCR loan.

What Is DSCR Loan?

DSCR loans are mortgage loans for residential, income-producing properties. These loans are mainly based on the Debt Service Coverage Ratio or DSCR, hence the name. Unlike conventional loans, DSCR loans are about the property’s income instead of the borrower’s

Baca Juga:

To be approved for a conventional loan, a borrower needs to provide income verification, a debt-to-income ratio, as well as tax returns. A DSCR loan Colorado requires none of these. As a result, they are attractive to real estate investors who are new in the industry and/or have limited financial resources.

What DSCR Loans Are for?

These loans are for real estate investors. They are ideal for investors in lots of diverse situations, From first-time real estate investors with little to no history to seasoned experts looking to scale their portfolio, all can benefit from DSCR loans.

What makes DSCR loans an even more attractive financing option is that they are a flexible solution with a relatively easy qualification. Especially so if compared to conventional loans which are stricter and much less flexible.

Baca Juga:

Who DSCR Loan Colorado Is for?

1. Freelancers or self-employed individuals looking to invest in real estate

It is quite difficult to qualify for conventional loans for investment properties if you don’t have a W-2. Traditional lenders will like to see a low debt-to-income and two years’ worth of income and employment for investors.

DSCR loans come with none of these. A W-2 income and a low DIT income are not necessary to qualify for a DSCR loan Colorado. Instead of using the personal income of the borrower as a qualification, DSCR loans use the potential income of the property.

Also Read:

Baca Juga:

- DSCR Loans Hawaii: Debt Service Coverage Ratio Loans

- DSCR Loans Michigan: Debt Service Coverage Ratio Loans

- DSCR Loan vs Conventional Loan: Which One is Better for You?

2. Individuals who invest in real estate with partners or a team

DSCR loans are undoubtedly an excellent option for those who invest in real estate with partners or a team. Investing in real estate with partners or a team often makes a lot of sense. After all, working with other individuals with skill sets that complement yours can go a long way.

For example, some investors may have the capital to invest in real estate but not time. Some others are the opposite, they have time and are willing to do the hard work of finding deals and managing properties. DSCR loans allow these investors to work together and achieve what they can do on their own.

3. Real estate investors pursuing niche strategies

Many real estate investors are using DSCR loans for straightforward rental properties. There are also some investors who are using DSCR loans for newer, niche strategies. Conventional loan lenders tend to frown upon such approaches as they are slow to adapt to new changes.

Baca Juga:

DSCR lenders, on the other hand, are more flexible and open to changes. This is especially true for lenders who are innovative and forward-thinking.

DSCR Loan Colorado Requirements

Some requirements must be met if a borrower is to qualify for a DSCR loan. Unlike conventional loans, however, the requirements to qualify for a DSCR loan are relatively less difficult to meet. Of course, that doesn’t mean there is no paperwork or documentation hurdle at all.

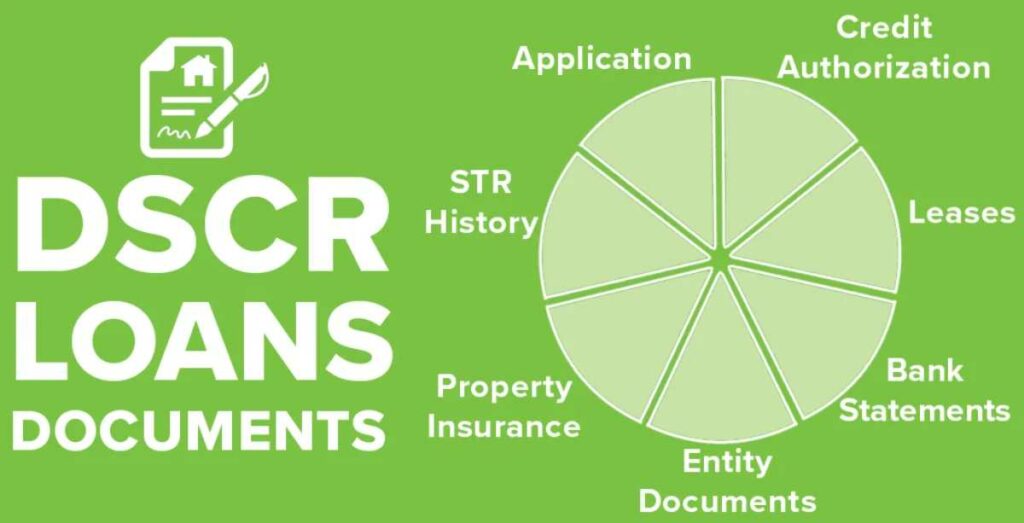

There is paperwork and documentation, but it is much lighter than that of conventional loans. Documentation is easy and non-burdensome. Here are the documentation requirements for a DSCR loan Colorado.

Baca Juga:

- Application. A loan application with some basic details on the borrower and property. Usually, it is only several pages long and takes about 15 minutes to finish.

- Credit authorization. An authorization form for the lender to run a background report and a credit report.

- Bank statements. You need to provide two months of bank statements showing that 3 to 6 months of liquid assets are available to cover any debt payments in case of turnover, vacancy, etc.

- Leases. If the property is a long-term rental, leases must be provided.

- Short-term rental history. If the property is used as a short-term rental and there are 12 months of operating history available.

- Insurance. Property insurance must be provided with the lender’s information included.

- Entity documents. This documentation is required if you choose to set up an LLC.

- Renovation documentation. If the borrower uses the loan for a quick cash-out refinance, documentation of the renovation work (work orders, invoices, receipts, etc.) may be required.

A DSCR loan Colorado is an excellent option for financing in a real estate investment. It is ideal not only for beginner investors who are just starting but also for experts who want to scale their portfolios.

Baca Juga: